Ever heard of FEMA? I’m sure in this post-Katrina age we live in that you have. The Federal Emergency Management Agency steps in to provide assistance when a disaster strikes somewhere in the US. But that’s not all. FEMA also offers the National Flood Insurance Program to provide coverage for people living in areas that are considered to be in a hazard zone for flooding. Participation in the flood insurance program is deemed mandatory when your property is in a Special Flood Hazard Area. With a standard annual premium of $1800 or more, even ‘if the creek don’t rise’ the cost of your insurance could surely drown you.

When I found my soon to be home I was taking a leisurely ride through a lovely older neighborhood here in Dallas. There was a creek to my right and we were approaching the lake that is near my office. It’s not a large lake and since Texas can be pretty arid and drought ridden I thought nothing of it. Only after we had started making offers on the home did I get an email from my loan officer mentioning the flood plain.

We pulled a flood cert and the property is in a flood zone. I would suggest that you investigate the costs of the additional coverage during your option period. Let me know if you want a referral to a great insurance agent.

Seeing as I’m with USAA, I passed on the referral and just called them. It took a while to get through to the Flood Department. This was right after the week that Mississippi had flooded so I wasn’t surprised to be waiting on hold. The hold wasn’t too bad and the agent was articulate and competent. Pat was her name.

Pat asked me a ton of questions about the elevation and it became clear I didn’t know any of the answers. I was trying to figure them out from the survey documents or “plat” that I had been sent from my loan officer. When it came down to it, Pat told me she was just going to punch in a bunch of general standards. After much todo and fussing a quote finally popped out and she read it to me: $1852 a year.

It really didn’t register with me that this was actually higher than the homeowners insurance quote I had been given. You see, flood insurance is an additional policy added to, and usually managed by, your homeowners insurance carrier. The coverage comes from FEMA and the cost is not controlled by who you get your quote from. After Pat explained all of this, my understanding was that this was a non negotiable price. This was very bad news.

The good news for me was that my Realtor had seen this before and he suggested I look into an elevation certificate. What’s that, you say? Well I’ll tell you. The elevation certificate is an official document created by the US Department of Homeland Security to determine the proper insurance premium rate for flood. Yet another agency I wasn’t thinking would be involved in my home buying process. I already have a redress number from the DHS since my name is similar to that of a known terrorist, so I wasn’t all that surprised to see them on letterhead. It was one of those, ‘so we meet again’ moments.

![]() In 1968 the federal government started the National Flood Insurance Plan, NFIP, because the probability of flood was so limited to certain areas, and the amount of possible damage so high, the risk level was unacceptable and therefore US insurance carriers were unable to spread the risk out enough to lower the cost of coverage. So the government stepped in. Love him or hate him, Uncle Sam is just trying to help. But let’s not get off topic.

In 1968 the federal government started the National Flood Insurance Plan, NFIP, because the probability of flood was so limited to certain areas, and the amount of possible damage so high, the risk level was unacceptable and therefore US insurance carriers were unable to spread the risk out enough to lower the cost of coverage. So the government stepped in. Love him or hate him, Uncle Sam is just trying to help. But let’s not get off topic.

I set about to order an elevation certificate by searching on Google. The best prices I found were around $350. Without thinking about it, I ordered one and handed over my debit card number. I pleaded with them to hurry it and I was told they could probably turn it around in 48 hours. The seven day option period can make you frantic if you let it. I texted my other half with an update. He called me back:

Me: I ordered an elevation cert. It was $350 and they can have it back in 2 days.

Him: Can you hold off on that?

Me: I’m just trying to get this handled within our option period! The agent said ‘the clock is ticking’ and we have seven days. I don’t want to lose that escrow money. ($1500 in my case)

Him: Don’t you think the title company could handle that?

I called my agent and asked him to see if he could order an elevation certificate through the title company. It turned out he could and that it only costs $275 when they do it. Another benefit of using the title company is that this cost isn’t due until closing. It may seem trivial that the money is due now or later, but when you’re trying to close on a house one of the processes in play is referred to as ‘proving income’ and it basically means having bank statements from your checking account(s) show as large of available balances as possible. Saving $75 on any single item in this process is like stopping another small leak in the dam.

Not being able to spend any money from your primary account(s) has the effect of feeling like your accounts are frozen. I just completed a week long stay at the beach without buying any new clothes for it. I’ve had maybe one visit to Starbucks a week and that’s off a gift card I already had. Given the additional $154 a month for flood insurance, we’ve been trying to see where we can tighten up our belts. There have been less visits to restaurants and many more sandwiches consumed. The good news is that this totally reminded me that what’s important in life are the experiences, not so much the stuff.

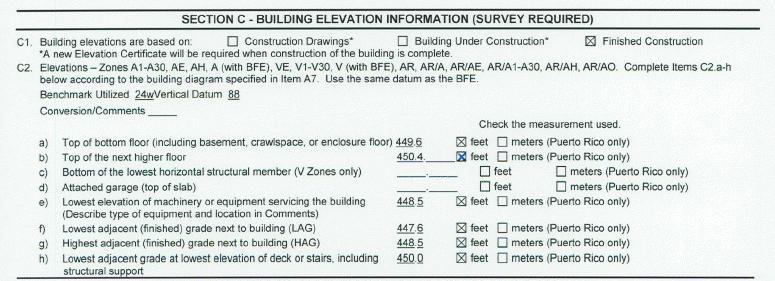

The elevation certificate came back rather quickly and I called my insurance provider again. The certificate has lettered sections with numbered subsections with lettered subsections. It’s really confusing to do over the phone. It came down to C 2a and C 2b which appear as follows:

If these fields are blank, which one of mine was, then the insurance agent will either not accept the form or start playing with the numbers moving them around “to get it to actually quote.” This isn’t what you want. She played with the numbers and got varying yearly premiums from $1800, $1300 and even $800. She told me that we should get the surveyor to put the correct values in and then we would know for sure.

I called the surveyor and he was able to get values into all these fields and email me an updated form. I had asked USAA for an email address to send the document to so that they could read it first hand. I was on vacation when it came back and so I logged into my email and sent the form off without really reviewing it very closely. I crossed my fingers hoping for that lucrative $800 per year rate. I didn’t hear back from them. Or so I thought.

When I got back to work this last Monday I had a voice mail waiting. Thinking it was someone asking me to do something when I was out of town, I put it low on my list to check these messages. 160 work emails later when I was all caught up, I dialed my voice mail system. Pat had left me a message from the day I had emailed them the amended elevation certificate. My new annual premium for flood insurance was a mere $452 per year. That’s $37.67 a month, like a cool ocean breeze blowing through my bank account.